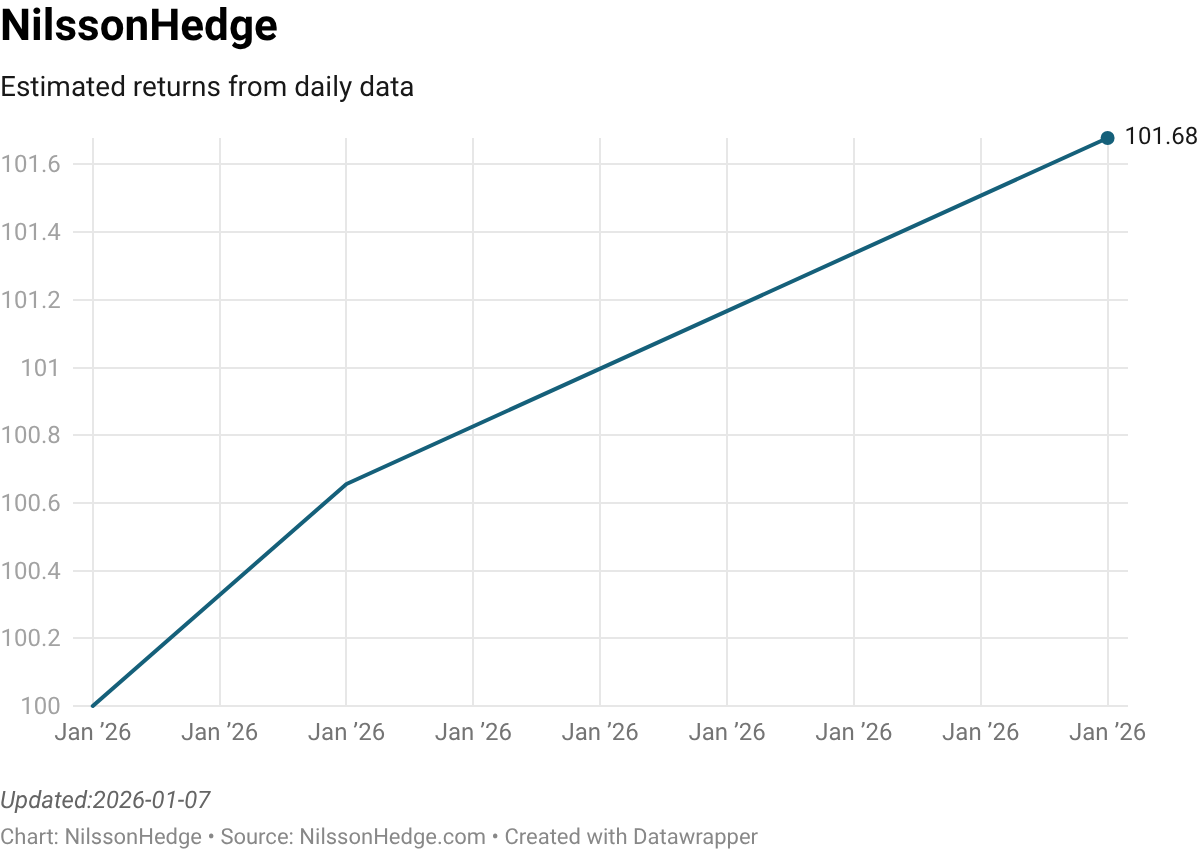

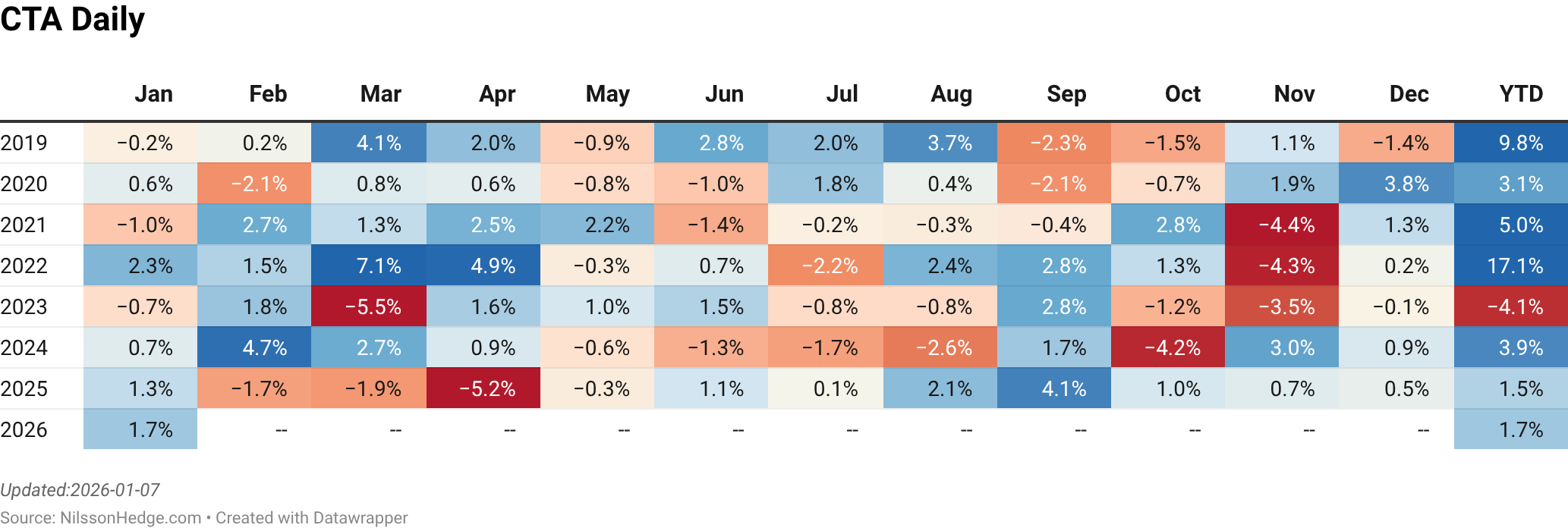

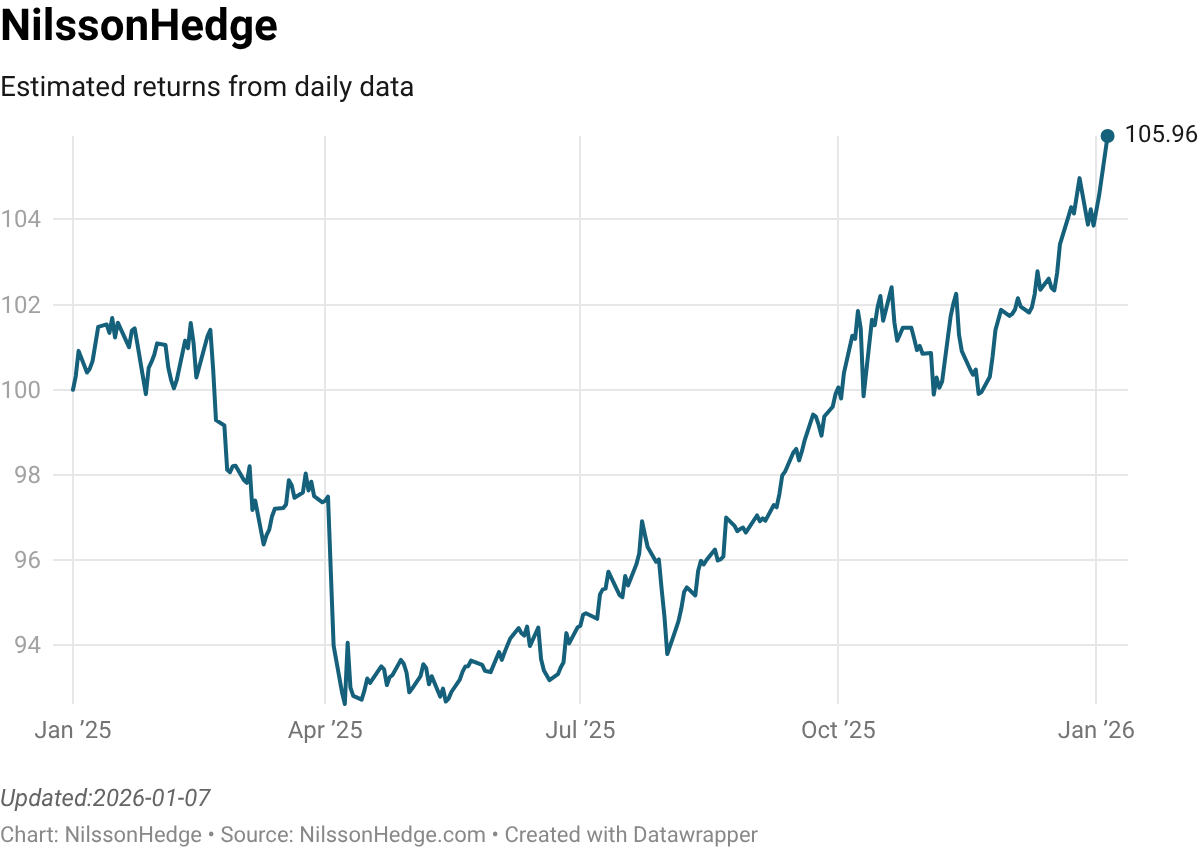

NilssonHedge provides a Daily CTA/Managed Futures index, based on the average returns for managers providing daily return data.

The managers included in the index are based on strategies that we have identified as consisting of Managed Futures funds (or using similar strategies) reporting Daily Numbers. Most of the managers are diversified across styles and sectors while others are focused on a particular sector. Some of them deploy leverage, to offset the risk reduction that a multiple return source allocation typically implies.

The managers included in the index are based on strategies that we have identified as consisting of Managed Futures funds (or using similar strategies) reporting Daily Numbers. Most of the managers are diversified across styles and sectors while others are focused on a particular sector. Some of them deploy leverage, to offset the risk reduction that a multiple return source allocation typically implies.

From Jan 1st, 2020 the index discloses constituents. The Index should be used as an indication of performance and general direction of pnl. The index is updated daily, without any manual checks. Thus the data may not be consistent over time and contain errors. The index does not adjust for different fee levels or entry/exit fees.

We do not impose minimum requirements on track records or aum for this subset. Managers that drop out of the index are replaced with the average return of the index.

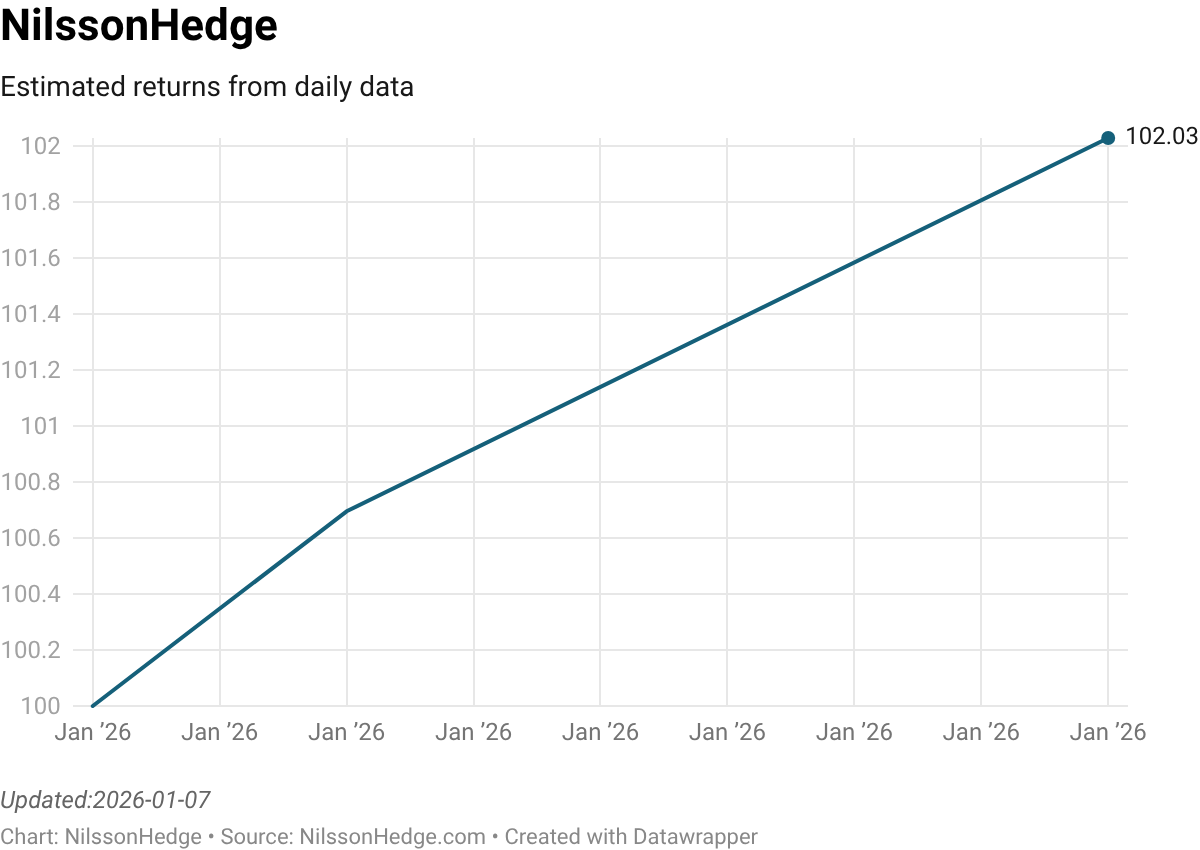

Daily CTA ETF Index

Based on the same methodology, we also created a CTA ETF index. The launch date is 2026-01-01, but the performance data contains backtracked information for 2025 for research purposes.

Methodology

In line with our method to build the database, we collect data from a large number of sources. A difference to monthly data is that we need to process daily returns much more carefully, apply filters and aggregate differently.

- Data is collected daily. One of the many problems with daily data is that is not cleaned in the same manner and may contain noise.

- To remove noise, for instance, driven by dividend payments that are not properly incorporated into the return stream, we take the median return over many share classes. This removes some of the spikes, but not all of them.

- Moreover, we apply a statistical filter to remove outliers. Here, we control market movements that cause the filter to remove true market returns. An example of this is, for instance, the CHF intervention in 2015, which caused large losses for several currency managers.

- As we aggregate over share classes and most managers only show the “cheapest” share class in their official track-record, our returns tend to show a lower rate of return and potentially more volatility.

- As part of our final statistical test, we correlate the equivalent monthly returns, from daily compounded returns, with monthly returns streams that already exist in the monthly database.

- Entry and Exit fees are ignored.

Index Constituents

| Abbey Capital | Abbey Capital Futures Strategy |

|---|---|

| Abbey Capital | Abbey Capital Multi Asset |

| ABR | Dynamic Short Volatility Fund |

| Altegris Advisors | Evolution Strategy |

| AQR Capital Management | AQR Managed Futures |

| AQR Capital Management | AQR Managed Futures HV Strategy |

| Campbell & Company | Managed Futures |

| Chesapeake Capital Corporation | Equinox Chesapeake Strategy |

| Credit Suisse Asset Management | Managed Futures Strategy Fund |

| Dunn Capital Management | Managed Futures Strategy (Arrow) |

| Goldman Sach Management | Goldman Sachs Mngd Futures Strat Instl |

| Graham Capital Mgmt LP | Tactical Trend |

| Guggenheim | Guggenheim Managed Futures Strategy |

| GuidePath | Managed Futures Strat |

| JHancock Diversified Macro Fund | jdjix JHancock Diversified Macro Fund |

| LoCorr Fund Management | LoCorr Macro Strategies |

| LoCorr Fund Management | Long/Short Commodity Strats |

| Man AHL | American Beacon AHL Mgd Futs Strat Instl |

| Natixis ASG | ASG |

| PIMCO | Trends Composite |

| Rational Advisors | Rational/ReSolve Adaptive Asset Allc |

| Redwood Systematic Macro Trnd (SMarT) Fd | Redwood Systematic Macro Trnd (SMarT) Fd |

| Standpoint Multi-Asset Fund | Standpoint Multi-Asset Fund |

ETFs

| AHL MF ETF | AHLT AHL MF ETF |

|---|---|

| Chesapeak Pure Trend ETF | MFUT Chesapeak Pure Trend ETF |

| Invesco MF ETF | IMF Invesco MF ETF |

| Chesapeak Managed Futures ETF | TFPN Chesapeak Managed Futures ETF |

| Fidelity Managed Futures ETF | FFUT Fidelity Managed Futures ETF |

| Ishares Managed Futures ETF | ISMF Ishares Managed Futures ETF |

| AlphaSimplex Managed Futures ETF | ASMF AlphaSimplex Managed Futures ETF |

| MTLucas Managed Futures ETF | KMLM MTLucas Managed Futures ETF |

| Return Stacked Portable Alpha ETF | FUTS Return Stacked Portable Alpha ETF |

| Wisdomtree Dynamic ETF | WDTI Wisdomtree Dynamic ETF |

| Wisdomtree Managed Futures ETF | WTMF Wisdomtree Managed Futures ETF |

| Unlimited Managed Futures ETF | FMF Unlimited Managed Futures ETF |

| Simplify Managed Futures ETF | CTA Simplify Managed Futures ETF |

| Dynamic Beta CTA ETF | DBMF Dynamic Beta CTA ETF |

| Abbey Capital | Abbey Capital Futures Strategy |

| Abbey Capital | Abbey Capital Multi Asset |

| ABR | Dynamic Short Volatility Fund |

| Altegris Advisors | Evolution Strategy |

| AQR Capital Management | AQR Managed Futures |

| AQR Capital Management | AQR Managed Futures HV Strategy |

| Campbell & Company | Managed Futures |

| Chesapeake Capital Corporation | Equinox Chesapeake Strategy |

| Credit Suisse Asset Management | Managed Futures Strategy Fund |

| DoubleLine | Multi-Asset Trend |

| Dunn Capital Management | Managed Futures Strategy (Arrow) |

| Fidelity | Macro Opps |

| Goldman Sach Management | Goldman Sachs Mngd Futures Strat Instl |

| Graham Capital Mgmt LP | Tactical Trend |

| Guggenheim | Guggenheim Managed Futures Strategy |

| GuidePath | Managed Futures Strat |

| JHancock Diversified Macro Fund | JHancock Diversified Macro Fund |

| LoCorr Fund Management | LoCorr Macro Strategies |

| LoCorr Fund Management | Long/Short Commodity Strats |

| Man AHL | American Beacon AHL Mgd Futs Strat Instl |

| Natixis ASG | ASG |

| PGIM Wadhwani Systematic Absolute Return | PGIM Wadhwani Systematic Absolute Return |

| PIMCO | Trends Composite |

| Rational Advisors | Rational/ReSolve Adaptive Asset Allc |

| Redwood Systematic Macro Trnd (SMarT) Fd | Redwood Systematic Macro Trnd (SMarT) Fd |

| Standpoint Multi-Asset Fund | Standpoint Multi-Asset Fund |

| Abbey Capital | Abbey Capital Multi Asset |

| ABR | Dynamic Short Volatility Fund |

| Altegris Advisors | Evolution Strategy |

| AQR Capital Management | AQR Managed Futures |

| AQR Capital Management | AQR Managed Futures HV Strategy |

| Campbell & Company | Managed Futures |

| Chesapeake Capital Corporation | Equinox Chesapeake Strategy |

| Credit Suisse Asset Management | Managed Futures Strategy Fund |

| DoubleLine | Multi-Asset Trend |

| DoubleLine Multi-Asset Trend Fund | DoubleLine Multi-Asset Trend Fund |

| Dunn Capital Management | Managed Futures Strategy (Arrow) |

| Fidelity | Macro Opps |

| FS Investments | Managed Futures |

| Goldman Sach Management | Goldman Sachs Mngd Futures Strat Instl |

| Graham Capital Mgmt LP | Tactical Trend |

| Guggenheim | Guggenheim Managed Futures Strategy |

| GuidePath | Managed Futures Strat |

| JHancock Diversified Macro Fund | JHancock Diversified Macro Fund |

| LoCorr Fund Management | LoCorr Macro Strategies |

| LoCorr Fund Management | Long/Short Commodity Strats |

| Longboard | Managed Futures Strategy |

| Man AHL | American Beacon AHL Mgd Futs Strat Instl |

| Natixis ASG | ASG |

| PGIM Wadhwani Systematic Absolute Return | PGIM Wadhwani Systematic Absolute Return |

| PIMCO | Trends Composite |

| Rational Advisors | Rational/ReSolve Adaptive Asset Allc |

| Redwood Systematic Macro Trnd (SMarT) Fd | Redwood Systematic Macro Trnd (SMarT) Fd |

| Standpoint Multi-Asset Fund | Standpoint Multi-Asset Fund |

| Superfund Capital Management | Managed Futures Strategy 40act |

Abbey Capital Abbey Capital Futures Strategy

Altegris Advisors Evolution Strategy

AQR Capital Management AQR Global Macro Fund

AQR Capital Management AQR Managed Futures

AQR Capital Management AQR Managed Futures HV Strategy

Catalyst Capital Advisors Multi-Strategy

Credit Suisse Asset Management Managed Futures Strategy Fund

Dorsey Wright DWA Tactical

Dunn Capital Management Managed Futures Strategy (Arrow)

FS Investments Managed Futures

Graham Capital Mgmt LP Tactical Trend

Guggenheim Guggenheim Managed Futures Strategy

Campbell & Company Managed Futures

GuidePath Managed Futures Strat

Man AHL American Beacon AHL Mgd Futs Strat Instl

LoCorr Fund Management LoCorr Macro Strategies

LoCorr Fund Management Long/Short Commodity Strats

JHancock Diversified Macro Fund JHancock Diversified Macro Fund

Longboard Managed Futures Strategy

PIMCO Em Mkts Ccy and S/T Invsmt

PIMCO Trends Composite

Rational Advisors Rational/ReSolve Adaptive Asset Allc

Superfund Capital Management Managed Futures Strategy 40act

USA Mutuals USA Mutuals Navigator Institutional

Virtus FORT Trend Fund Virtus FORT Trend Fund

| Abbey Capital | Abbey Capital Futures Strategy |

| Abbey Capital | Abbey Capital Multi Asset |

| Man AHL | American Beacon AHL Mgd Futs Strat Instl |

| AQR Capital Management | AQR Managed Futures |

| AQR Capital Management | AQR Managed Futures HV Strategy |

| Natixis ASG | ASG |

| Standpoint Multi-Asset Fund | Multi-Asset Fund |

| DoubleLine Multi-Asset Trend Fund | Multi-Asset Trend Fund |

| Chesapeake Capital Corporation | Equinox Chesapeake Strategy |

| Altegris Advisors | Evolution Strategy |

| Goldman Sach Management | Goldman Sachs Mngd Futures Strat Instl |

| Guggenheim | Guggenheim Managed Futures Strategy |

| JHancock Diversified Macro Fund | JHancock Diversified Macro Fund |

| JHancock Alternative Risk Premia Fund | JHancock Alternative Risk Premia Fund |

| LoCorr Fund Management | LoCorr Macro Strategies |

| LoCorr Fund Management | Long/Short Commodity Strats |

| James Alpha | Macro |

| Campbell & Company | Managed Futures |

| FS Investments | Managed Futures |

| GuidePath | Managed Futures Strat |

| Longboard | Managed Futures Strategy |

| Dunn Capital Management | Managed Futures Strategy (Arrow) |

| Superfund Capital Management | Managed Futures Strategy 40act |

| Credit Suisse Asset Management | Managed Futures Strategy Fund |

| Catalyst Capital Advisors | Multi-Strategy |

| Equinox Fund Management | MutualHedge Futures Strategy |

| PGIM Wadhwani Systematic Absolute Return | PGIM Wadhwani Systematic Absolute Return |

| Rational Advisors | Rational/ReSolve Adaptive Asset Allc |

| Redwood Systematic Macro Trnd (SMarT) Fd | Redwood Systematic Macro Trnd (SMarT) Fd |

| Graham Capital Mgmt LP | Tactical Trend |

| PIMCO | Trends Composite |

| Virtus FORT Trend Fund | Virtus FORT Trend Fund |

| 361 Capital | 361 Global Managed Futures Strategy Fund |

| 361 Capital | 361 Managed Futures Strategy Fund |

| Abbey Capital | Abbey Capital Futures Strategy |

| Altegris Advisors | Evolution Strategy |

| AQR Capital Management | AQR Managed Futures |

| AQR Capital Management | AQR Managed Futures HV Strategy |

| Aspect Capital Limited | Aspect Core Trend Fund |

| Campbell & Company | Campbell Dynamic Trend Fund |

| Campbell & Company | Managed Futures |

| Catalyst Capital Advisors | Multi-Strategy |

| Chesapeake Capital Corporation | Equinox Chesapeake Strategy |

| Credit Suisse Asset Management | Managed Futures Strategy Fund |

| Dorsey Wright | DWA Tactical |

| Dunn Capital Management | Managed Futures Strategy (Arrow) |

| Equinox Fund Management | Equinox Ampersand Strategy Fund |

| Equinox Fund Management | MutualHedge Futures Strategy |

| FS Investments | Managed Futures |

| Goldman Sach Management | Goldman Sachs Mngd Futures Strat Instl |

| Graham Capital Mgmt LP | Tactical Trend |

| Guggenheim | Guggenheim Managed Futures Strategy |

| GuidePath | Managed Futures Strat |

| James Alpha | Macro |

| JHancock | Absolute Return Currency |

| LoCorr Fund Management | LoCorr Macro Strategies |

| LoCorr Fund Management | Long/Short Commodity Strats |

| Longboard | Managed Futures Strategy |

| Man AHL | American Beacon AHL Mgd Futs Strat Instl |

| PanAgora Asset Management | PanAgora Managed Futures Strategy |

| PIMCO | Em Mkts Ccy and S/T Invsmt |

| PIMCO | Trends Composite |

| Rational Advisors | Rational/ReSolve Adaptive Asset Allc |

| Superfund Capital Management | Managed Futures Strategy 40act |

| USA Mutuals | USA Mutuals Navigator Institutional |

| Virtus FORT Trend Fund | Virtus FORT Trend Fund |

| 361 Capital | 361 Global Managed Futures Strategy Fund |

| 361 Capital | 361 Managed Futures Strategy Fund |

| Abbey Capital | Abbey Capital Futures Strategy |

| Allianz Global Investors | AllianzGI Managed Futures Strategy |

| Altegris Advisors | Managed Futures |

| AQR Capital Management | AQR Managed Futures |

| AQR Capital Management | AQR Managed Futures HV Strategy |

| Aspect Capital Limited | Aspect Core Trend Fund |

| Campbell & Company | Managed Futures |

| Campbell & Company | Campbell Dynamic Trend Fund |

| Catalyst Capital Advisors | Multi-Strategy |

| Chesapeake Capital Corporation | Equinox Chesapeake Strategy |

| Credit Suisse Asset Management | Managed Futures Strategy Fund |

| Dorsey Wright | DWA Tactical |

| Dunn Capital Management | Managed Futures Strategy (Arrow) |

| Equinox Fund Management | MutualHedge Futures Strategy |

| FS Investments | Managed Futures |

| Goldman Sach Management | Goldman Sachs Mngd Futures Strat Instl |

| Graham Capital Mgmt LP | Tactical Trend |

| Gresham Investment Management | Managed Futures Strat |

| GSA Capital Partners | GSA Trend Fund |

| GuidePath | Managed Futures Strat |

| IPM Informed Portfolio Management | IPM Systematic Macro |

| James Alpha | Macro |

| LoCorr Fund Management | LoCorr Macro Strategies |

| LoCorr Fund Management | Long/Short Commodity Strats |

| Man AHL | American Beacon AHL Mgd Futs Strat Instl |

| PanAgora Asset Management | PanAgora Managed Futures Strategy |

| PIMCO | Trends Composite |

| Rational Advisors | Rational/ReSolve Adaptive Asset Allc |

| Steben | Managed Futures Strategy |