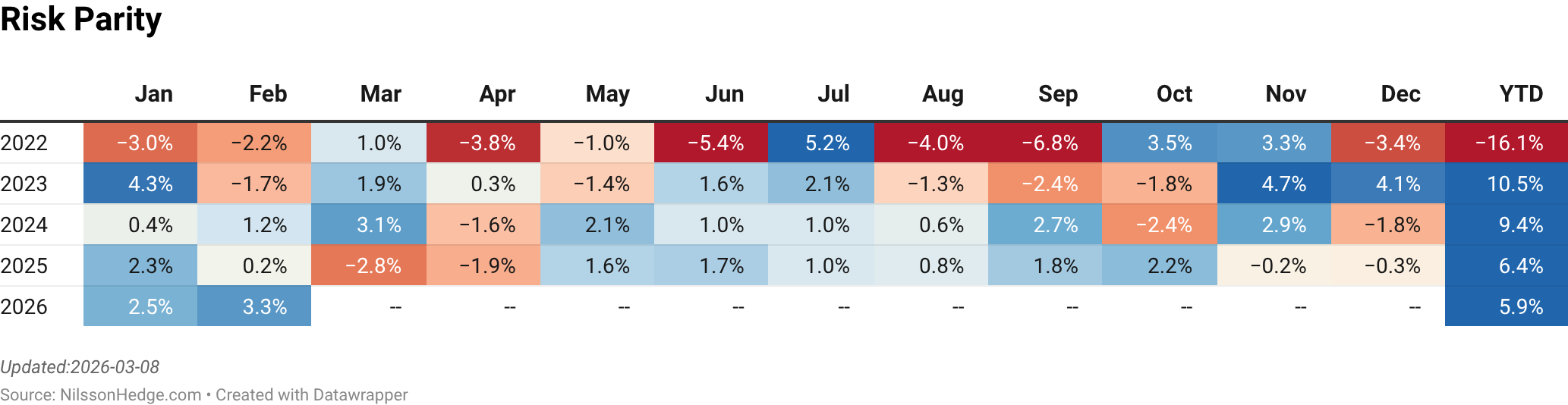

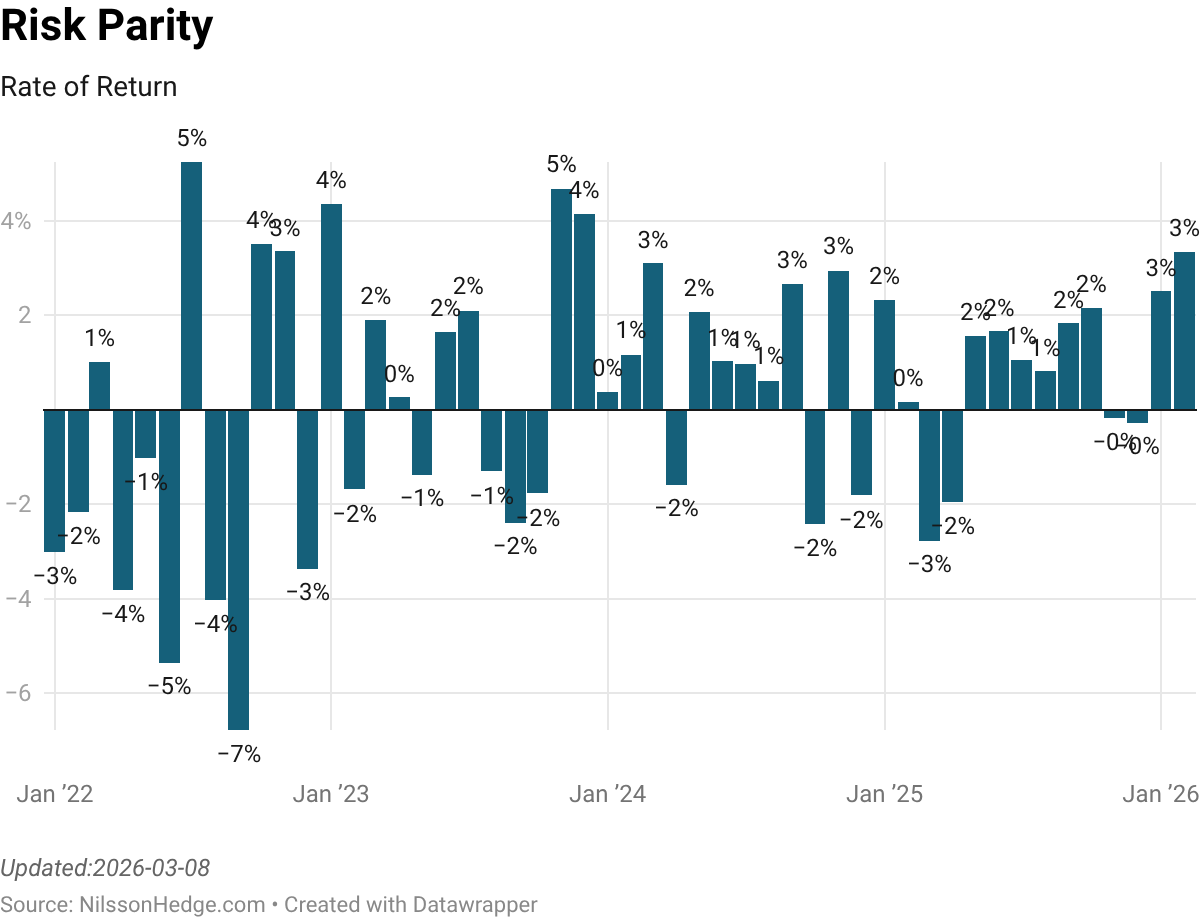

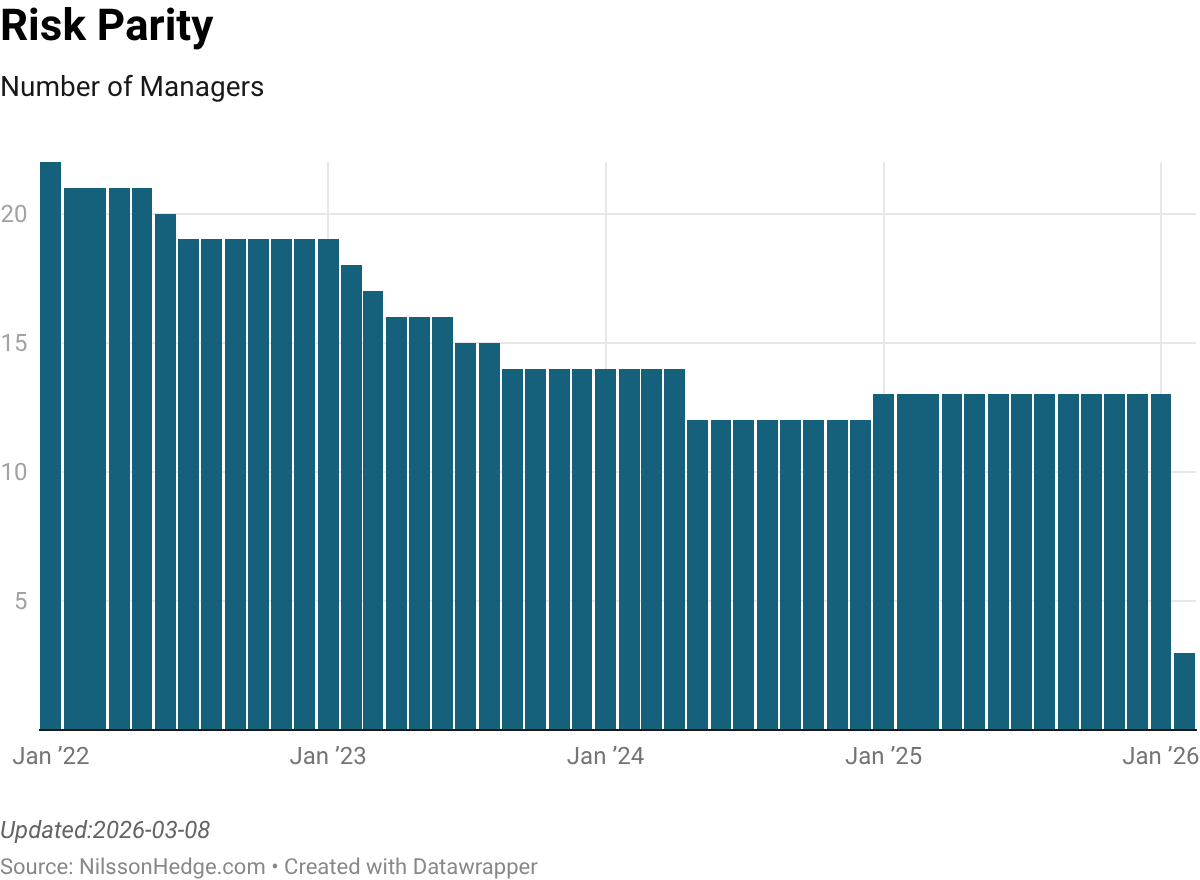

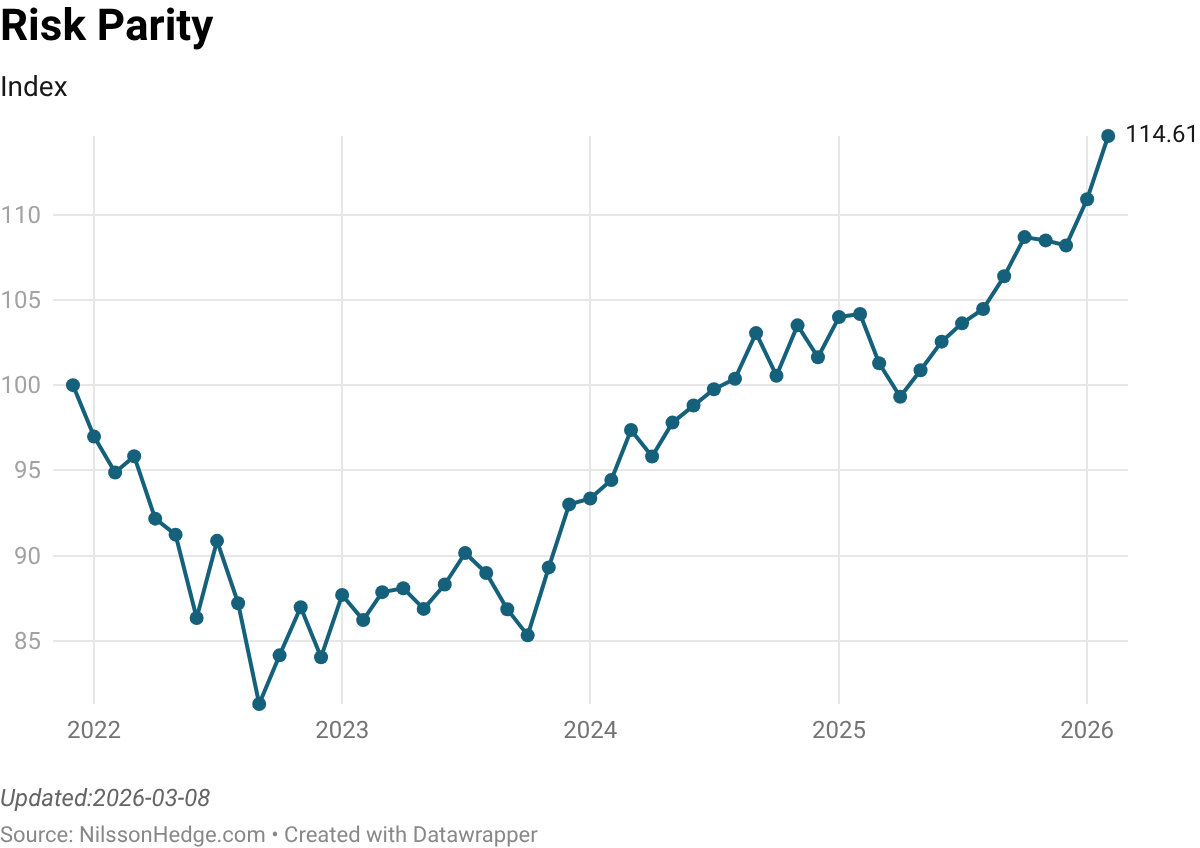

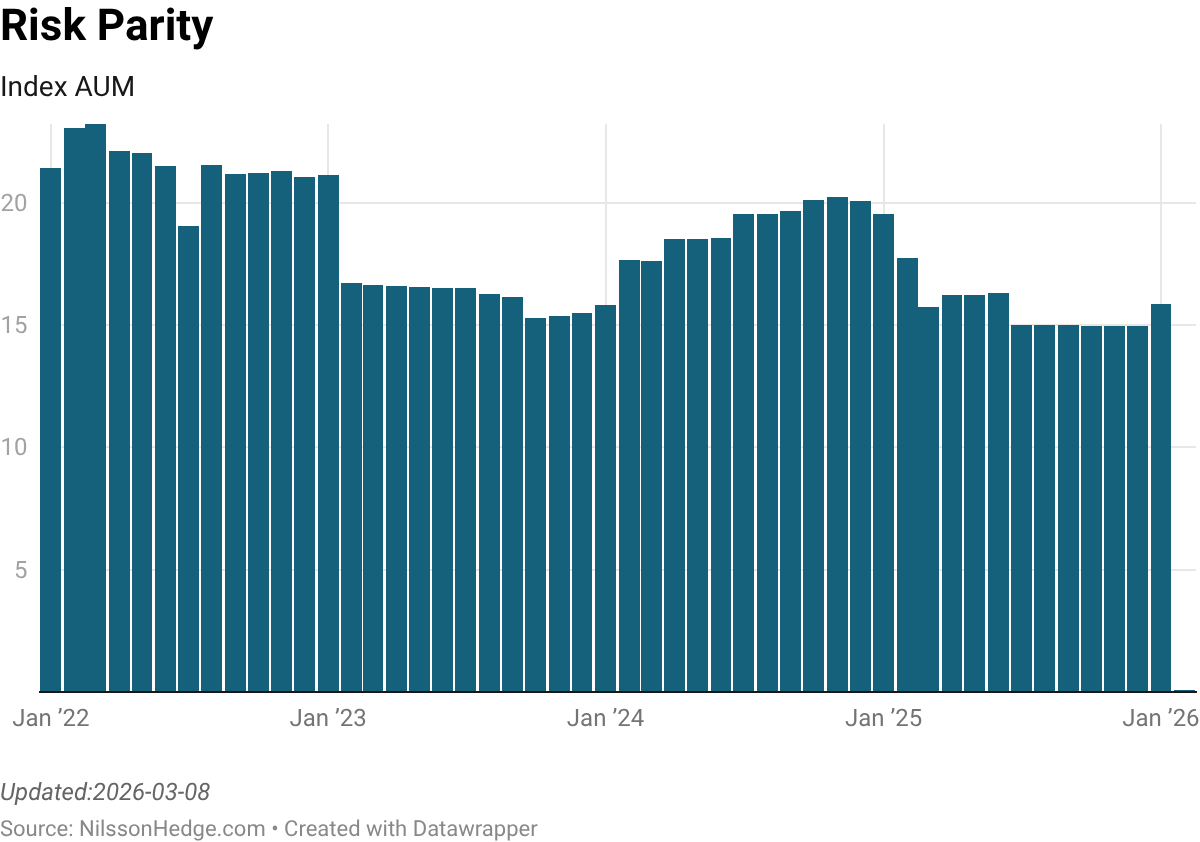

NilssonHedge provides a Risk Parity Index, based on the average returns of the underlying managers. We do not provide backtracked returns nor do we allow for “instant track records”. Managers are included if they existed in the database, in December, of the prior year.

Risk Parity portfolios are based on the notion that most asset classes have the same expected risk-adjusted returns. If that is indeed the case, the rational approach is to balance the expected risk and use the correlation benefits to achieve a higher risk-adjusted return. In some cases, managers differentiate between Volatility and Risk Parity where the former only focuses on risk for each asset class, whereas the latter also adds a correlation structure.

Risk Parity portfolios are typically either (modestly) leveraged or have lower volatility than pure equity portfolios. Volatility targeting a specific volatility target is also common. In most cases, this is a long-only portfolio with limited capabilities to enter short positions.

The index is based on managers that are part of the database as of the end of the prior year. We do not impose minimum requirements on track records or aum for this subset. Managers that drop out of the index are replaced with the average return of the index.

The purpose of the index is to track funds that are reporting data publically and may thus exclude certain managers that have chosen not to do so.

Constituents

| Manager | Program |

|---|---|

| AQR Capital Management | AQR Risk-Balanced Commodities Strategy |

| AQR Capital Management | Global Risk Parity |

| AQR Capital Management | Multi-Asset |

| Columbia Threadneedle | Columbia Adaptive Risk Allocation |

| Formuepleje Fund Management | Formuepleje Epikur |

| Formuepleje Fund Management | Formuepleje Pareto |

| Formuepleje Fund Management | Formuepleje Penta |

| Formuepleje Fund Management | Formuepleje Safe |

| Katonah Eve | Global Tactical Allocation Program |

| Lyxor | Arma 8 |

| Man AHL | AHL Target Growth |

| Man AHL | AHL TargetRisk Fund |

| Man AHL | Dynamic Allocation Fund |

| Sanlam | Managed Risk |

| Manager | Program |

|---|---|

| AQR Capital Management | Global Risk Parity |

| AQR Capital Management | Multi-Asset |

| Columbia Threadneedle | Columbia Adaptive Risk Allocation |

| Formuepleje Fund Management | Formuepleje Epikur |

| Formuepleje Fund Management | Formuepleje Pareto |

| Formuepleje Fund Management | Formuepleje Penta |

| Formuepleje Fund Management | Formuepleje Safe |

| Katonah Eve | Global Tactical Allocation Program |

| Lyxor | Arma 8 |

| Man AHL | AHL Target Growth |

| Man AHL | AHL TargetRisk Fund |

| Man AHL | Dynamic Allocation Fund |

| Sanlam | Managed Risk |

| Manager | Program |

|---|---|

| AQR Capital Management | AQR Risk-Balanced Commodities Strategy |

| AQR Capital Management | Global Risk Parity |

| AQR Capital Management | Multi-Asset |

| Bridgewater | All Weather |

| Columbia Threadneedle | Columbia Adaptive Risk Allocation |

| Formuepleje Fund Management | Formuepleje Epikur |

| Formuepleje Fund Management | Formuepleje Pareto |

| Formuepleje Fund Management | Formuepleje Penta |

| Formuepleje Fund Management | Formuepleje Safe |

| Katonah Eve | Global Tactical Allocation Program |

| Man AHL | AHL Target Growth |

| Man AHL | AHL TargetRisk Fund |

| Sanlam | Managed Risk |

| WH Asset Management | WH Index |

| Manager | Program |

|---|---|

| AQR Capital Management | Global Risk Parity |

| AQR Capital Management | Multi-Asset |

| Bridgewater | All Weather |

| Columbia Threadneedle | Columbia Adaptive Risk Allocation |

| Formuepleje Fund Management | Formuepleje Epikur |

| Formuepleje Fund Management | Formuepleje Pareto |

| Formuepleje Fund Management | Formuepleje Penta |

| Formuepleje Fund Management | Formuepleje Safe |

| Global Bayesian Dynamics | Risk Parity |

| Invesco | Balanced Risk 8 |

| Katonah Eve | Global Tactical Allocation Program |

| Lyxor | Arma 8 |

| Man AHL | AHL Target Growth |

| Man AHL | AHL TargetRisk Fund |

| Millburn Ridgefield Corporation | Adaptive Allocation Program |

| PanAgora | Risk Parity |

| Sanlam | Managed Risk |

| Securian AM | Dynamic Managed Vol |

| WH Asset Management | WH Index |

| Manager | Program |

|---|---|

| AQR Capital Management | Global Risk Parity |

| AQR Capital Management | Multi-Asset |

| Bridgewater | All Weather |

| Columbia Threadneedle | Columbia Adaptive Risk Allocation |

| First Quadrant LP | Balanced Risk Commodities |

| First Quadrant LP | Essential Beta |

| Focus Point Capital | FPC Macro |

| Formuepleje Fund Management | Formuepleje Epikur |

| Formuepleje Fund Management | Formuepleje Pareto |

| Formuepleje Fund Management | Formuepleje Penta |

| Formuepleje Fund Management | Formuepleje Safe |

| Global Bayesian Dynamics | Risk Parity |

| Invesco | Balanced Risk 8 |

| Katonah Eve | Global Tactical Allocation Program |

| Lyxor | Arma 8 |

| Man AHL | AHL Target Growth |

| Man AHL | AHL TargetRisk Fund |

| Millburn Ridegfield Corporation | Adaptive Allocation Program |

| PanAgora | Risk Parity |

| Sanlam | Managed Risk |

| Securian AM | Dynamic Managed Vol |

| WH Asset Management | WH Index |