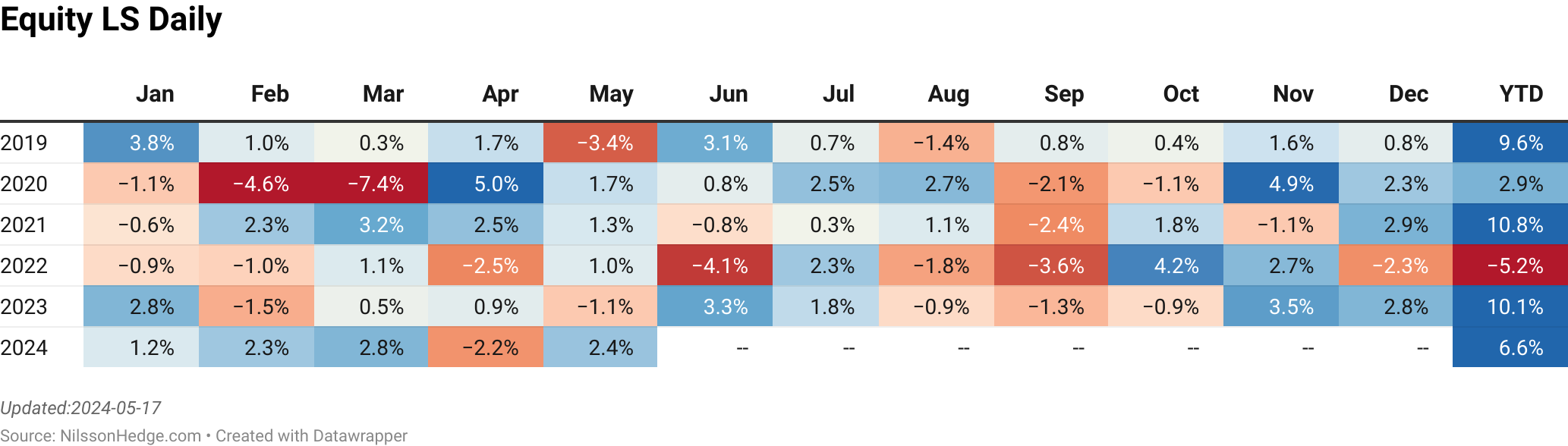

NilssonHedge provides a Daily Long-Short Equity index, based on the average returns of the underlying managers. This index is expected to be correlated to overall equity markets.

The managers included in the index are based on strategies that we have identified as consisting of Long-Short Equity funds (or using similar strategies) reporting Daily Numbers through liquid funds. Most of the managers are diversified across styles and sectors while others are focused on a particular sector. Most of the managers deploy long/short alpha strategies in US equity markets while some diversify into Global markets. Beta is the overarching risk factor.

From Jan 1st, 2020 we disclose index constituents. The Index should be used as an indication of performance and general direction of returns. The index is updated daily, without any manual checks. Thus the data may not be consistent over time and contain errors. The index does not adjust for different fee levels or entry/exit fees.

We do not impose minimum requirements on track records or asset under management for this subset. Managers that drop out of the index are replaced with the average return of the index.

Methodology

In line with our method to build the database, we collect data from a large number of sources. A difference to monthly data is that we need to process daily returns much more carefully, apply filters and aggregate differently.

- Data is collected daily. One of the many problems with daily data is that is not cleaned in the same manner and may contain noise.

- To remove noise, for instance, driven by dividend payments that are not properly incorporated into the return stream, we take the median return over many share classes. This removes some of the spikes, but not all of them.

- Moreover, we apply a statistical filter to remove outliers. Here, we control for market movements that cause the filter to remove true market returns.

- As we aggregate over share classes and most managers only show the “cheapest” share class in their official track record, our returns tend to show a lower rate of return and potentially more volatility.

- As part of our final statistical test, we correlate the equivalent monthly returns, from daily compounded returns, with monthly returns streams that already exist in the monthly database.

- Entry and Exit fees are ignored.

Index Constituents

| ABR | 50/50 Volatility Investor |

| ABR | 75/25 Volatility Fund |

| ABR | Dynamic Blend Equity & Volatil |

| Absolute Investment Adv | Capital Opportunities |

| ACM | Dynamic Opportunity |

| Alger | Dynamic Opportunities |

| AllianceBernstein | Select US Long/Short |

| AMG | Veritas Global Real Return |

| Anchor Capital | Anchor Risk Mgd Equity Strategies Adv |

| Anchor Capital | Tactical Equity Strategies |

| AQR Capital Management | Long-Short Equity |

| AQR Capital Management | Sustainable Long-Short Eq |

| BlackRock | U.S. Insights Long/Shrt Eq |

| Boston Partners | Boston Partners Emerging Mkts L/S |

| Boston Partners | Boston Partners Long/Short Equity |

| Boston Partners | Boston Partners Long/Short Rsrch |

| Calamos | Calamos Phineus Long/Short |

| Catalyst Funds | Nasdaq-100 Hedged Equity |

| Catalyst Funds | Systematic Alpha |

| Counterpoint | Counterpoint Tactical Equity |

| CRM | Long/Short Opportunities |

| Diamond Hill | Diamond Hill Long-Short |

| Easterly | Snow Capital Long/Short Opportunity Fund |

| Fintrust | Fintrust Income and Opportunity |

| First Quadrant LP | FQ Long-Short Equity |

| Forester | Forester Value |

| Glenmede | Quant US Long/Short Equity |

| Gotham | Gotham Absolute Return Institutional |

| Gotham | Gotham Total Return |

| Guggenheim | Guggenheim Alpha Opportunity |

| Highland | Highland Long/Short Healthcare |

| Invenomic Institutional | Invenomic Institutional |

| JPMorgan Equity Premium Income Fund | jeprx JPMorgan Equity Premium Income Fund |

| JPMorgan Hedged Equity Fund | jhqrx JPMorgan Hedged Equity Fund |

| Knights of Columbus Long/Short Equity Fd | kceix Knights of Columbus Long/Short Equity Fd |

| LoCorr Fund Management | Dynamic Equity |

| Longboard | Longboard Alternative Growth |

| LS Opportunity | LS Opportunity Fund |

| Marketfield | Marketfield |

| Meeder | Meeder Spectrum |

| MFS | MFS Managed Wealth |

| Neuberger Berman | Neuberger Berman Long Short |

| Nuveen | Nuveen Equity Long/Short |

| Parvin | Hedged Equity Solari World Fund |

| Persimmon | Persimmon Long/Short |

| PIMCO | PIMCO RAE Worldwide Long/Short PLUS |

| Rational | Equity Armor Fund |

| RiverPark | RiverPark Long/Short Opportunity |

| Salient | Salient Tactical Growth |

| Salient | Salient Tactical Plus |

| Snow Capital | Snow Capital Long/Short Opportunity |

| Toews | Toews Tactical Defensive Alpha |

| Toews | Toews Tactical Monument |

| Toews | Toews Tactical Oceana |

| Toews | Toews Tactical Opportunity |

| USA Mutuals | USA Mutuals Navigator Institutional |

| Wasatch | Long/Short Alpha Investor |

| Waycross | Waycross Long/Short Equity |

| Weitz Partners III | Weitz Partners III Opportunity |

| Wilmington | Wilmington Global Alpha Equities |

| BlackRock | Global Long/Short Equity |

| ABR | 75/25 Volatility Fund |

| 361 Capital | Global Long/Short Equity |

| ABR | 50/50 Volatility Investor |

| ABR | 75/25 Volatility Fund |

| ABR | Dynamic Blend Equity & Volatil |

| Absolute Investment Adv | Capital Opportunities |

| ACM | Dynamic Opportunity |

| Alger | Dynamic Opportunities |

| AllianceBernstein | Select US Long/Short |

| Allspring | Allspring Global Long/Short |

| AmericaFirst | AmericaFirst Defensive Growth |

| AMG | Veritas Global Real Return |

| Anchor Capital | Anchor Risk Mgd Equity Strategies Adv |

| Anchor Capital | Risk Mgd Global Strategies Adv |

| Anchor Capital | Tactical Equity Strategies |

| Anchor Capital | Tactical Global Strategies |

| AQR Capital Management | Long-Short Equity |

| AQR Capital Management | Sustainable Long-Short Eq |

| BlackRock | Global Equity Abs Rtn |

| BlackRock | U.S. Insights Long/Shrt Eq |

| BlackRock | Global Long/Short Equity |

| Boston Partners | Boston Partners Emerging Mkts L/S |

| Boston Partners | Boston Partners Long/Short Equity |

| Boston Partners | Boston Partners Long/Short Rsrch |

| Boston Partners | Partners Global Long/Short |

| Calamos | Calamos Phineus Long/Short |

| Caldwell & Orkin | Caldwell & Orkin – Gator Capital L/S |

| Catalyst Funds | Nasdaq-100 Hedged Equity |

| Catalyst Funds | Systematic Alpha |

| Counterpoint | Counterpoint Tactical Equity |

| CRM | Long/Short Opportunities |

| Diamond Hill | Diamond Hill Long-Short |

| Easterly | Snow Capital Long/Short Opportunity Fund |

| Fintrust | Fintrust Income and Opportunity |

| First Quadrant LP | FQ Long-Short Equity |

| Forester | Forester Value |

| Glenmede | Quant US Long/Short Equity |

| Gotham | Gotham Absolute Return Institutional |

| Gotham | Gotham Defensive Long 500 |

| Gotham | Gotham Hedged Core Institutional |

| Gotham | Gotham Total Return |

| Guggenheim | Guggenheim Alpha Opportunity |

| Guggenheim | Guggenheim Long Short Equity |

| Highland | Highland Long/Short Healthcare |

| Invenomic Institutional | Invenomic Institutional |

| JHancock | Seaport Long/Short |

| JPMorgan Equity Premium Income Fund | JPMorgan Equity Premium Income Fund |

| JPMorgan Hedged Equity Fund | JPMorgan Hedged Equity Fund |

| JPMorgan International Hedged Equity Fd | JPMorgan International Hedged Equity Fd |

| Knights of Columbus Long/Short Equity Fd | kceix Knights of Columbus Long/Short Equity Fd |

| LoCorr Fund Management | Dynamic Equity |

| Longboard | Longboard Alternative Growth |

| LS Opportunity | LS Opportunity Fund |

| Marketfield | Marketfield |

| Meeder | Meeder Spectrum |

| MFS | MFS Managed Wealth |

| Neuberger Berman | Neuberger Berman Long Short |

| Nuveen | Nuveen Equity Long/Short |

| Otter Creek | Otter Creek Long/Short Opportunity |

| Parvin | Hedged Equity Solari World Fund |

| Persimmon | Persimmon Long/Short |

| PIMCO | PIMCO RAE Worldwide Long/Short PLUS |

| Rational | Equity Armor Fund |

| RiverPark | RiverPark Long/Short Opportunity |

| Salient | Salient Tactical Growth |

| Salient | Salient Tactical Plus |

| Snow Capital | Snow Capital Long/Short Opportunity |

| Toews | Toews Tactical Defensive Alpha |

| Toews | Toews Tactical Monument |

| Toews | Toews Tactical Oceana |

| Toews | Toews Tactical Opportunity |

| USA Mutuals | USA Mutuals Navigator Institutional |

| Virtus KAR | Virtus KAR Long/Short Equity |

| Wasatch | Long/Short Alpha Investor |

| Waycross | Waycross Long/Short Equity |

| Weitz Partners III | Weitz Partners III Opportunity |

| Wilmington | Wilmington Global Alpha Equities |

| 361 Capital | Global Long/Short Equity |

| ABR | 75/25 Volatility Fund |

| ABR | Dynamic Blend Equity & Volatil |

| Absolute Investment Adv | Capital Opportunities |

| ACM | Dynamic Opportunity |

| Alger | Dynamic Opportunities |

| AllianceBernstein | Select US Long/Short |

| Allspring | Allspring Global Long/Short |

| Allspring | Allspring U.S. Long/Short Equity |

| AmericaFirst | AmericaFirst Defensive Growth |

| AMG | River Road Long-Short |

| AMG | Veritas Global Real Return |

| Anchor Capital | Anchor Risk Mgd Equity Strategies Adv |

| Anchor Capital | Risk Mgd Global Strategies Adv |

| Anchor Capital | Tactical Equity Strategies |

| Anchor Capital | Tactical Global Strategies |

| AQR Capital Management | Long-Short Equity |

| AQR Capital Management | Sustainable Long-Short Eq |

| AXS Multi-Strategy Alternatives Fund | AXS Multi-Strategy Alternatives Fund |

| BlackRock | Global Equity Abs Rtn |

| BlackRock | U.S. Insights Long/Shrt Eq |

| Boston Partners | Boston Partners Emerging Mkts L/S |

| Boston Partners | Boston Partners Long/Short Equity |

| Boston Partners | Boston Partners Long/Short Rsrch |

| Boston Partners | Partners Global Long/Short |

| Calamos | Calamos Phineus Long/Short |

| Caldwell & Orkin | Caldwell & Orkin – Gator Capital L/S |

| Catalyst Funds | Systematic Alpha |

| Counterpoint | Counterpoint Tactical Equity |

| CRM | Long/Short Opportunities |

| Delaware | Hedged U.S. Equity Opps Instl |

| Diamond Hill | Diamond Hill Long-Short |

| Easterly | Snow Capital Long/Short Opportunity Fund |

| Fintrust | Fintrust Income and Opportunity |

| First Quadrant LP | FQ Long-Short Equity |

| Forester | Forester Value |

| Glenmede | Quant US Long/Short Equity |

| Global Tactical Fund | Global Tactical Fund |

| Gotham | Gotham Absolute Return Institutional |

| Gotham | Gotham Defensive Long 500 |

| Gotham | Gotham Hedged Core Institutional |

| Gotham | Gotham Total Return |

| Guggenheim | Guggenheim Alpha Opportunity |

| Guggenheim | Guggenheim Long Short Equity |

| Highland | Highland Long/Short Healthcare |

| Invenomic Institutional | Invenomic Institutional |

| Invenomic Investor | Invenomic Institutional |

| Invenomic Super Institutional | Invenomic Institutional |

| JHancock | Hancock Seaport Long/Short |

| JHancock | Seaport Long/Short |

| JPMorgan Equity Premium Income Fund | JPMorgan Equity Premium Income Fund |

| JPMorgan Hedged Equity Fund | JPMorgan Hedged Equity Fund |

| JPMorgan International Hedged Equity Fd | JPMorgan International Hedged Equity Fd |

| Knights of Columbus Long/Short Equity Fd | Knights of Columbus Long/Short Equity Fd |

| LoCorr Fund Management | Dynamic Equity |

| Longboard | Longboard Alternative Growth |

| LS Opportunity | LS Opportunity Fund |

| Marketfield | Marketfield |

| Meeder | Meeder Spectrum |

| MFS | MFS Managed Wealth |

| Multi-Manager | Multi-Manager Directional Alt Strat |

| Navigator | Navigator Equity Hedged |

| Neuberger Berman | Neuberger Berman Long Short |

| Nuance | Nuance Concentrated Value L-S |

| Nuveen | Nuveen Equity Long/Short |

| Otter Creek | Otter Creek Long/Short Opportunity |

| Parvin | Hedged Equity Solari World Fund |

| Persimmon | Persimmon Long/Short |

| PIMCO | PIMCO RAE Worldwide Long/Short PLUS |

| Rational | Equity Armor Fund |

| RiverPark | RiverPark Long/Short Opportunity |

| Salient | Salient Tactical Growth |

| Salient | Salient Tactical Plus |

| Sirios | Sirios Long/Short |

| Snow Capital | Snow Capital Long/Short Opportunity |

| Toews | Toews Tactical Defensive Alpha |

| Toews | Toews Tactical Monument |

| Toews | Toews Tactical Oceana |

| Toews | Toews Tactical Opportunity |

| USA Mutuals | USA Mutuals Navigator Institutional |

| Virtus KAR | Virtus KAR Long/Short Equity |

| Wasatch | Long/Short Alpha Investor |

| Waycross | Waycross Long/Short Equity |

| Weitz Partners III | Weitz Partners III Opportunity |

| Wilmington | Wilmington Global Alpha Equities |

Virtus KAR Virtus KAR Long/Short Equity

Waycross Waycross Long/Short Equity

Weitz Partners III Weitz Partners III Opportunity

Wilmington Wilmington Global Alpha Equities

Sirios Sirios Long/Short

The Covered Bridge Fund tcbix The Covered Bridge Fund

Toews Toews Tactical Defensive Alpha

Toews Toews Tactical Monument

Toews Toews Tactical Oceana

Toews Toews Tactical Opportunity

Salient Salient Tactical Growth

Salient Salient Tactical Plus

Securian AM Securian AM Managed Volatility Eq

RiverPark RiverPark Long/Short Opportunity

Snow Capital Snow Capital Long/Short Opportunity

Probabilities Probabilities

PIMCO PIMCO RAE Worldwide Long/Short PLUS

Persimmon Persimmon Long/Short

MFS MFS Managed Wealth

Nuance Nuance Concentrated Value L-S

Nuveen Nuveen Equity Long/Short

Otter Creek Otter Creek Long/Short Opportunity

Meeder Meeder Spectrum

JPMorgan JPMorgan Opportunistic Equity L/S

JHancock Hancock Seaport Long/Short

JPMorgan Equity Premium Income Fund jeprx JPMorgan Equity Premium Income Fund

JPMorgan Hedged Equity Fund jhqrx JPMorgan Hedged Equity Fund

JPMorgan International Hedged Equity Fd jihrx JPMorgan International Hedged Equity Fd

Knights of Columbus Long/Short Equity Fd kceix Knights of Columbus Long/Short Equity Fd

Longboard Longboard Alternative Growth

LoCorr Fund Management Dynamic Equity

Marketfield Marketfield

LS Opportunity LS Opportunity Fund

Multi-Manager Multi-Manager Directional Alt Strat

Natixis ASG ASG

Navigator Navigator Equity Hedged

Neuberger Berman Neuberger Berman Long Short

Highland Highland Long/Short Healthcare

Invenomic Institutional Invenomic Institutional

Invenomic Investor Invenomic Institutional

Invenomic Super Institutional Invenomic Institutional

Hussman Strategic Growth Hussman Strategic Growth

Hussman Strategic International Hussman Strategic International

Glenmede Quant US Long/Short Equity

Gotham Gotham Total Return

Guggenheim Guggenheim Alpha Opportunity

Guggenheim Guggenheim Long Short Equity

Gotham Gotham Absolute Return Institutional

Gotham Gotham Defensive Long 500

Gotham Gotham Hedged Core Institutional

Gotham Gotham Hedged Plus Institutional

Fintrust Fintrust Income and Opportunity

First Quadrant LP FQ Long-Short Equity

Forester Forester Value

CRM Long/Short Opportunities

Diamond Hill Diamond Hill Long-Short

Counterpoint Counterpoint Tactical Equity

Causeway Causeway Global Absolute Return Instl

Clough Global Clough Global Long/Short

BlackRock Global Long/Short Equity

Boston Partners Boston Partners Emerging Mkts L/S

Boston Partners Boston Partners Long/Short Equity

Boston Partners Boston Partners Long/Short Rsrch

Boston Partners Partners Global Long/Short

Calamos Calamos Phineus Long/Short

Caldwell & Orkin Caldwell & Orkin – Gator Capital L/S

Beacon Accelerated Return Strategy Fund barlx Beacon Accelerated Return Strategy Fund

Beacon Planned Return Strategy Fund bprlx Beacon Planned Return Strategy Fund

Arin Large Cap Theta Fund avolx Arin Large Cap Theta Fund

AQR Capital Management Long-Short Equity

ABR Dynamic Blend Equity & Volatil

AmericaFirst AmericaFirst Defensive Growth

AMG River Road Long-Short

Anchor Capital Tactical Equity Strategies

Anchor Capital Tactical Global Strategies

361 Capital Domestic Long/Short Equity

361 Capital Global Long/Short Equity

ACM Dynamic Opportunity

Absolute Investment Adv Capital Opportunities

AllianceBernstein Select US Long/Short

Alger Dynamic Opportunities

| 361 Capital | Domestic Long/Short Equity |

| 361 Capital | Global Long/Short Equity |

| ABR | Dynamic Blend Equity & Volatil |

| Absolute Investment Adv | Capital Opportunities |

| ACM | Dynamic Opportunity |

| Alger | Dynamic Opportunities |

| AllianceBernstein | Select US Long/Short |

| AmericaFirst | AmericaFirst Defensive Growth |

| AMG | River Road Long-Short |

| Anchor Capital | Tactical Equity Strategies |

| Anchor Capital | Tactical Global Strategies |

| AQR Capital Management | Long-Short Equity |

| AXS Multi-Strategy Alternatives Fund | AXS Multi-Strategy Alternatives Fund |

| Boston Partners | Boston Partners Emerging Mkts L/S |

| Boston Partners | Boston Partners Long/Short Equity |

| Boston Partners | Boston Partners Long/Short Rsrch |

| Boston Partners | Partners Global Long/Short |

| Calamos | Calamos Phineus Long/Short |

| Caldwell & Orkin | Caldwell & Orkin – Gator Capital L/S |

| Catalyst Funds | Systematic Alpha |

| Clough Global | Clough Global Long/Short |

| Counterpoint | Convergence Long/Short Equity |

| Counterpoint | Counterpoint Tactical Equity |

| CRM | Long/Short Opportunities |

| Diamond Hill | Diamond Hill Long-Short |

| Equinox Fund Management | Equinox Ampersand Strategy Fund |

| Fintrust | Fintrust Income and Opportunity |

| First Quadrant LP | FQ Long-Short Equity |

| Forester | Forester Value |

| FS Investments | Long/Short Equity |

| Gabelli | Mergers & Acquisitions |

| Glenmede | Quant US Long/Short Equity |

| Global Tactical Fund | Global Tactical Fund |

| Gotham | Gotham Absolute Return Institutional |

| Gotham | Gotham Defensive Long 500 |

| Gotham | Gotham Hedged Core Institutional |

| Gotham | Gotham Hedged Plus Institutional |

| Gotham | Gotham Total Return |

| Guggenheim | Guggenheim Alpha Opportunity |

| Guggenheim | Guggenheim Long Short Equity |

| Hancock Horizon | Hancock Horizon Quant Long/Short |

| Highland | Highland Long/Short Healthcare |

| Invenomic Institutional | Invenomic Institutional |

| Invenomic Investor | Invenomic Institutional |

| Invenomic Super Institutional | Invenomic Institutional |

| James Alpha | James Alpha EHS Portfolio |

| JHancock | Hancock Seaport Long/Short |

| JPMorgan | JPMorgan Opportunistic Equity L/S |

| JPMorgan Equity Premium Income Fund | jeprx JPMorgan Equity Premium Income Fund |

| JPMorgan Hedged Equity Fund | jhqrx JPMorgan Hedged Equity Fund |

| JPMorgan International Hedged Equity Fd | jihrx JPMorgan International Hedged Equity Fd |

| Knights of Columbus Long/Short Equity Fd | kceix Knights of Columbus Long/Short Equity Fd |

| LoCorr Fund Management | Dynamic Equity |

| Longboard | Longboard Alternative Growth |

| LS Opportunity | LS Opportunity Fund |

| Marketfield | Marketfield |

| Meeder | Meeder Spectrum |

| MFS | MFS Managed Wealth |

| Multi-Manager | Multi-Manager Directional Alt Strat |

| Navigator | Navigator Equity Hedged |

| Neuberger Berman | Neuberger Berman Long Short |

| Nuance | Nuance Concentrated Value L-S |

| Nuveen | Nuveen Equity Long/Short |

| Otter Creek | Otter Creek Long/Short Opportunity |

| Persimmon | Persimmon Long/Short |

| PGIM QMA | PGIM QMA Long-Short Equity |

| PIMCO | PIMCO RAE Worldwide Long/Short PLUS |

| Probabilities | Probabilities |

| RiverPark | RiverPark Long/Short Opportunity |

| Salient | Salient Tactical Growth |

| Salient | Salient Tactical Plus |

| Scharf | Scharf Alpha Opportunity |

| Securian AM | Securian AM Managed Volatility Eq |

| Sirios | Sirios Long/Short |

| Snow Capital | Snow Capital Long/Short Opportunity |

| Thornburg | Thornburg Long/Short Equity |

| Toews | Toews Tactical Defensive Alpha |

| Toews | Toews Tactical Monument |

| Toews | Toews Tactical Oceana |

| Toews | Toews Tactical Opportunity |

| USA Mutuals | USA Mutuals Navigator Institutional |

| Virtus KAR | Virtus KAR Long/Short Equity |

| Water Island Long/Short Fund | atqix Water Island Long/Short Fund |

| Waycross | Waycross Long/Short Equity |

| Weitz Partners III | Weitz Partners III Opportunity |

| Wilmington | Wilmington Global Alpha Equities |

| 361 Capital | Domestic Long/Short Equity |

| 361 Capital | Global Long/Short Equity |

| ABR | Dynamic Blend Equity & Volatil |

| Absolute Investment Adv | Capital Opportunities |

| ACM | Dynamic Opportunity |

| Alger | Dynamic Opportunities |

| AllianceBernstein | Select US Long/Short |

| AmericaFirst | AmericaFirst Defensive Growth |

| AMG | River Road Long-Short |

| Anchor Capital | Tactical Equity Strategies |

| Anchor Capital | Tactical Global Strategies |

| AQR Capital Management | Long-Short Equity |

| Arin Large Cap Theta Fund | Arin Large Cap Theta Fund |

| AXS Multi-Strategy Alternatives Fund | AXS Multi-Strategy Alternatives Fund |

| AXS Multi-Strategy Alternatives Fund | AXS Multi-Strategy Alternatives Fund |

| Balter European | European L/S Small Cap |

| Beacon Accelerated Return Strategy Fund | Beacon Accelerated Return Strategy Fund |

| Beacon Planned Return Strategy Fund | Beacon Planned Return Strategy Fund |

| BlackRock | Global Long/Short Equity |

| Boston Partners | Boston Partners Emerging Mkts L/S |

| Boston Partners | Boston Partners Long/Short Equity |

| Boston Partners | Boston Partners Long/Short Rsrch |

| Boston Partners | Partners Global Long/Short |

| Calamos | Calamos Phineus Long/Short |

| Caldwell & Orkin | Caldwell & Orkin – Gator Capital L/S |

| Causeway | Causeway Global Absolute Return Instl |

| Clough Global | Clough Global Long/Short |

| Counterpoint | Convergence Long/Short Equity |

| Counterpoint | Counterpoint Tactical Equity |

| CRM | Long/Short Opportunities |

| Diamond Hill | Diamond Hill Long-Short |

| Diamond Hill | Diamond Hill Research Opportunities |

| Fintrust | Fintrust Income and Opportunity |

| First Quadrant LP | FQ Long-Short Equity |

| Forester | Forester Value |

| FS Investments | Long/Short Equity |

| Glenmede | Quant US Long/Short Equity |

| Gotham | Gotham Absolute 500 Core |

| Gotham | Gotham Absolute 500 Institutional |

| Gotham | Gotham Absolute Return Institutional |

| Gotham | Gotham Defensive Long 500 |

| Gotham | Gotham Defensive Long Institutional |

| Gotham | Gotham Hedged Core Institutional |

| Gotham | Gotham Hedged Plus Institutional |

| Gotham | Gotham Total Return |

| Guggenheim | Guggenheim Alpha Opportunity |

| Guggenheim | Guggenheim Long Short Equity |

| Hancock Horizon | Hancock Horizon Quant Long/Short |

| Highland | Highland Long/Short Healthcare |

| Hussman Strategic Growth | Hussman Strategic Growth |

| Hussman Strategic International | Hussman Strategic International |

| Invenomic Institutional | Invenomic Institutional |

| Invenomic Investor | Invenomic Institutional |

| Invenomic Super Institutional | Invenomic Institutional |

| James Alpha | James Alpha EHS Portfolio |

| James Alpha | James Alpha Relative Value |

| JHancock | Hancock Seaport Long/Short |

| JPMorgan | JPMorgan Opportunistic Equity L/S |

| JPMorgan Equity Premium Income Fund | JPMorgan Equity Premium Income Fund |

| JPMorgan Hedged Equity Fund | JPMorgan Hedged Equity Fund |

| JPMorgan International Hedged Equity Fd | JPMorgan International Hedged Equity Fd |

| JPMorgan Macro Opportunities Fund | JPMorgan Macro Opportunities Fund |

| JPMorgan Macro Opportunities Fund | JPMorgan Macro Opportunities Fund |

| Knights of Columbus | Long/Short Equity Fund |

| LoCorr Fund Management | Dynamic Equity |

| Longboard | Longboard Alternative Growth |

| LS Opportunity | LS Opportunity Fund |

| Main BuyWrite Fund | Main BuyWrite Fund |

| Marketfield | Marketfield |

| Meeder | Meeder Spectrum |

| MFS | MFS Managed Wealth |

| Midwood Long/Short Equity Fund | Midwood Long/Short Equity Fund |

| Multi-Manager | Multi-Manager Directional Alt Strat |

| Natixis ASG | ASG |

| Navigator | Navigator Equity Hedged |

| Navigator Sentry | Navigator Sentry Managed Volatility |

| Neuberger Berman | Neuberger Berman Long Short |

| Nuance | Nuance Concentrated Value L-S |

| Nuveen | Nuveen Equity Long/Short |

| Otter Creek | Otter Creek Long/Short Opportunity |

| Persimmon | Persimmon Long/Short |

| PGIM QMA | PGIM QMA Long-Short Equity |

| PIMCO | PIMCO RAE Worldwide Long/Short PLUS |

| Probabilities | Probabilities |

| RiverPark | RiverPark Long/Short Opportunity |

| Salient | Salient Tactical Growth |

| Salient | Salient Tactical Plus |

| Scharf | Scharf Alpha Opportunity |

| Schwab | Schwab Hedged Equity |

| Securian AM | Securian AM Managed Volatility Eq |

| Sirios | Sirios Long/Short |

| Snow Capital | Snow Capital Long/Short Opportunity |

| The Covered Bridge Fund | The Covered Bridge Fund |

| Thornburg | Thornburg Long/Short Equity |

| Toews | Toews Tactical Defensive Alpha |

| Toews | Toews Tactical Monument |

| Toews | Toews Tactical Oceana |

| Toews | Toews Tactical Opportunity |

| Virtus KAR | Virtus KAR Long/Short Equity |

| Waycross | Waycross Long/Short Equity |

| Weitz Partners III | Weitz Partners III Opportunity |

| Wilmington | Wilmington Global Alpha Equities |

| 361 Capital | Domestic Long/Short Equity |

| 361 Capital | Global Long/Short Equity |

| ABR | Dynamic Blend Equity & Volatil |

| Absolute Investment Adv | Capital Opportunities |

| ACM | Dynamic Opportunity |

| Alger | Dynamic Opportunities |

| AllianceBernstein | Select US Long/Short |

| AmericaFirst | AmericaFirst Defensive Growth |

| American Century | Discp Long Short |

| AMG | River Road Long-Short |

| Anchor Capital | Tactical Equity Strategies |

| Anchor Capital | Tactical Global Strategies |

| AQR Capital Management | Long-Short Equity |

| Balter European | European L/S Small Cap |

| BlackRock | Global Long/Short Equity |

| BMO | Global Long/Short Equity |

| Boston Partners | Boston Partners Emerging Mkts L/S |

| Boston Partners | Boston Partners Long/Short Equity |

| Boston Partners | Boston Partners Long/Short Rsrch |

| Boston Partners | Partners Global Long/Short |

| Calamos | Calamos Phineus Long/Short |

| Caldwell & Orkin | Caldwell & Orkin – Gator Capital L/S |

| Causeway | Causeway Global Absolute Return Instl |

| Clough Global | Clough Global Long/Short |

| Counterpoint | Convergence Long/Short Equity |

| Counterpoint | Counterpoint Tactical Equity |

| CRM | Long/Short Opportunities |

| Diamond Hill | Diamond Hill Long-Short |

| Diamond Hill | Diamond Hill Research Opportunities |

| Fintrust | Fintrust Income and Opportunity |

| First Quadrant LP | FQ Long-Short Equity |

| Forester | Forester Value |

| FS Investments | Long/Short Equity |

| Glenmede | Quant US Long/Short Equity |

| Gotham | Gotham Absolute 500 Core |

| Gotham | Gotham Absolute 500 Institutional |

| Gotham | Gotham Absolute Return Institutional |

| Gotham | Gotham Defensive Long 500 |

| Gotham | Gotham Defensive Long Institutional |

| Gotham | Gotham Hedged Core Institutional |

| Gotham | Gotham Hedged Plus Institutional |

| Gotham | Gotham Total Return |

| Guggenheim | Guggenheim Alpha Opportunity |

| Guggenheim | Guggenheim Long Short Equity |

| Hancock Horizon | Hancock Horizon Quant Long/Short |

| Highland | Highland Long/Short Equity |

| Highland | Highland Long/Short Healthcare |

| Hussman Strategic Growth | Hussman Strategic Growth |

| Hussman Strategic International | Hussman Strategic International |

| Invesco | Invesco Long/Short Equity |

| James Alpha | James Alpha EHS Portfolio |

| James Alpha | James Alpha Relative Value |

| JHancock | Hancock Seaport Long/Short |

| JPMorgan | JPMorgan Opportunistic Equity L/S |

| LoCorr Fund Management | Dynamic Equity |

| Longboard | Longboard Alternative Growth |

| LS Opportunity | LS Opportunity Fund |

| Marketfield | Marketfield |

| Meeder | Meeder Spectrum |

| MFS | MFS Managed Wealth |

| MProved Systematic | MProved Systematic Long-Short |

| Multi-Manager | Multi-Manager Directional Alt Strat |

| Nationwide | Nationwide Long/Short Equity |

| Natixis ASG | Natixis ASG Tactical US Market |

| Navigator | Navigator Equity Hedged |

| Neuberger Berman | Neuberger Berman Long Short |

| Nuance | Nuance Concentrated Value L-S |

| Nuveen | Nuveen Equity Long/Short |

| Otter Creek | Otter Creek Long/Short Opportunity |

| Persimmon | Persimmon Long/Short |

| PGIM QMA | PGIM QMA Long-Short Equity |

| PIMCO | PIMCO Eq Long/Short |

| PIMCO | PIMCO RAE Worldwide Long/Short PLUS |

| Probabilities | Probabilities |

| Pzena | Pzena Long/Short Value |

| RMB Mendon | Mendon Financial Long/Short |

| Salient | Salient Tactical Growth |

| Salient | Salient Tactical Plus |

| Scharf | Scharf Alpha Opportunity |

| Schwab | Schwab Hedged Equity |

| Securian AM | Securian AM Managed Volatility Eq |

| Sirios | Sirios Long/Short |

| Snow Capital | Snow Capital Long/Short Opportunity |

| Thornburg | Thornburg Long/Short Equity |

| Toews | Toews Tactical Defensive Alpha |

| Toews | Toews Tactical Monument |

| Toews | Toews Tactical Oceana |

| Toews | Toews Tactical Opportunity |

| Virtus KAR | Virtus KAR Long/Short Equity |

| Waycross | Waycross Long/Short Equity |

| Weitz Partners III | Weitz Partners III Opportunity |

| Wilmington | Wilmington Global Alpha Equities |