The Long/Short Equity strategy is probably the oldest hedge fund strategy, established by the legendary Alfred Winslow Jones who created the first widely recognized hedge fund. His partnership was a strategy that sought to hedge out market risk (not all, but part of it) by matching long picks with a selection of short picks that were expected to reduce equity market risk. He used leverage aggressively but hedged with short positions in a way that according to him used “speculative techniques for conservative ends”.

Long/Short Equity funds tend to be long-biased, i.e. they partly depend on the overall direction of the equity market but also through the stock-picking capabilities of the manager. It has sometimes been described as “double alpha” as the manager should, in theory, be able to earn returns on both the long and short views. That is however seldom true and like a lot of other liquid strategies, most of the returns originated from the long side. Over the last decade, short-selling has been a particularly painful exercise.

You can view Equity Long/Short as an unconstrained mutual fund where the manager is not restricted from value creation through tracking a particular index, with a long-only restriction.

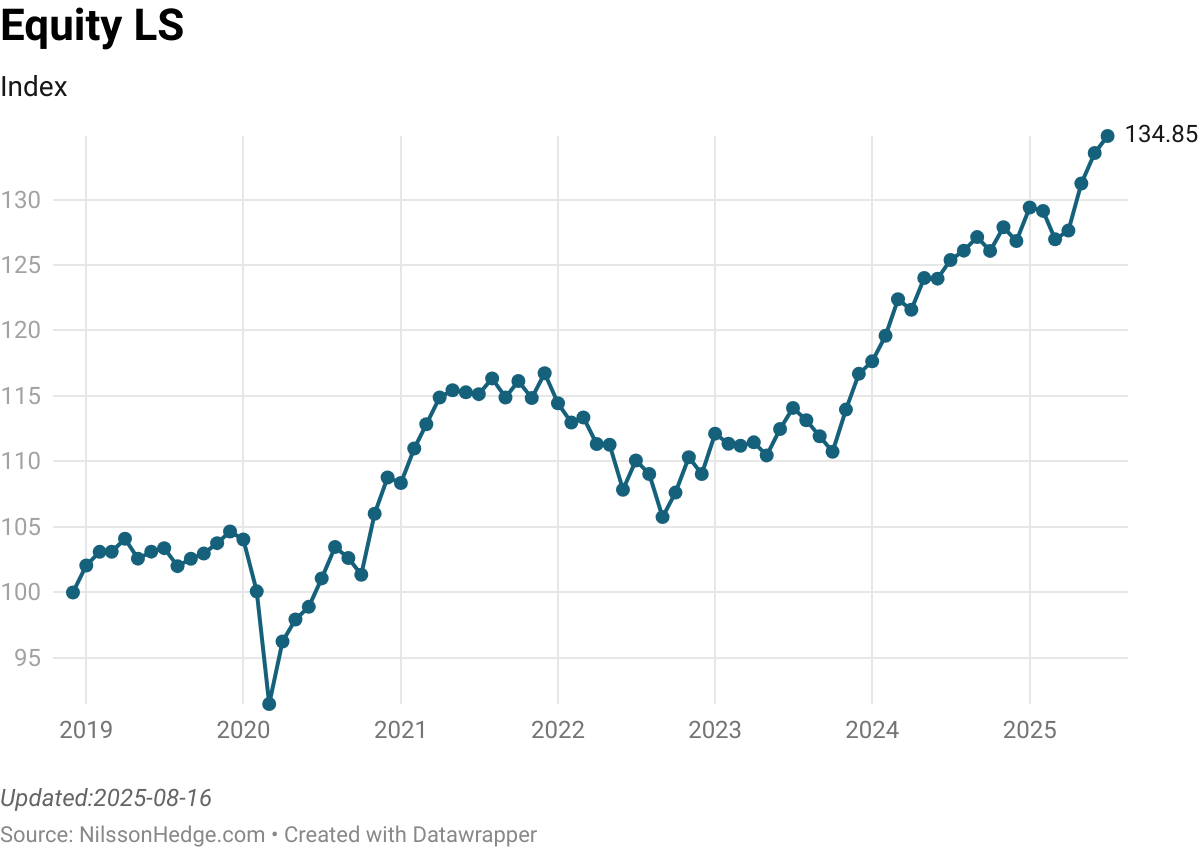

Long/Short equity funds come in a large number of different flavors where one of the differentiators is the amount of equity market risk that is accepted by the different funds. On average, equity market risk is close to one-half, and relatively little diversification can be achieved against the broader equity markets. NilssonHedge tracks daily beta and correlation for long/short equity strategies based on our daily composite.

Hedging the long exposure can take many shapes and forms. Occasionally the longs are hedged with a relative value view on a similar stock, while at other times the exposure is hedged with Futures or ETFs. Moreover, the beta of any fund can be variable, if the manager is trying to time the overall market direction. The different ways to hedge the long book result in slightly different risk profiles. With shorts expressed via specific stocks, the fund will be more exposed to so-called “idiosyncratic” events (i.e. GameStop, Volkswagen) than a short via an index hedge. Unfortunately, an index hedge can also expose the manager to competitive pressure as there is no attempt to generate returns from the short side. While index shorts may ultimately be a better way to hedge, it also increases the commercial risk for the manager.

Understanding and evaluating a long/short strategy is straightforward, the markets are easy to understand and the investment process is often discretionary (sometimes with the support of systematic screens). Adjusted for risk, is the manager able to outperform a given benchmark and if so, is the underlying process transparent.

Risk

The maximum drawdown for the strategy is often driven by the standard deviation of the strategy. Most funds, with a track record longer than a few years, will have experienced a maximum drawdown that is around 2x the standard deviation of the strategy. Furthermore, given the almost explicit market risk, there is a considerable co-movement with equities. An investor needs to carefully watch specifics for a particular manager. A concentrated manager may have higher volatility and performance expectations, but this comes at a higher risk of suffering from stock-specific drawdowns.

Our Resources

NilssonHedge has multiple resources available to allow you to analyze long/short equity managers. We have two different performance indicators (a daily, and a monthly), correlation monitors, and our latest addition, a manager dispersion tool that allows you to answer if your manager is above or below your expectations.

You must be logged in to post a comment.